During lockdown I wrote a weekly email covering the important news from the tech sector, summarised and placed in the Irish context. It kept me sane during lockdown, but I paused in 2021 once I started a new job (writing tech policy at TTC Labs).

I’ve missed it dearly, so now I’m resuming the newsletter but with a different topic – the Irish Political Economy. In a similar format as before, I’ll be looking at the week’s major stories in the Irish and Global economy, trying to put them in context and exploring how government policy can help.

If that’s your cup of tea, you can subscribe here. I hope you’ll enjoy!

Why are Car Rental Prices Skyrocketing?

Maybe you’ve seen this tweet from CNN’s Donie O’Sullivan, being quoted almost €2k for renting a car while he’s home in Ireland for a week.

Or you’ve heard stories like this one from my friend Eoin Hayes, whose brother was quoted €10k for a 3 week rental.

€10k is approximately the same price I paid for my Volkswagen Polo, only I got mine for keeps!

To put it mildly, this is wild. It will also potentially have some knock-on effects on the number of tourists who can afford to visit the island this summer.

It’s presumably all COVID related, but what exactly is going on? Why is it more acute in Ireland than other areas? What are the options for getting it fixed and how long will that take?

Is it Price Gouging?

Some of the initial public comments have been to accuse the car rental companies of price gouging. In most other areas of pandemic-related-inflation it is true that many businesses are using the current supply constraints to increase their profits. Still, I don’t think it’s accurate to say that corporate greed *caused* the problem. Many businesses have always been greedy, and they’re certainly *exploiting* the current situation, but their greed didn’t cause it.

There are 13 large car rental companies in Ireland. If greed alone would let them raise prices, they would have done it years ago. Something fundamental has changed to allow them all do this in unison.

A good rule of thumb with inflation is that price rises are the symptom, not the cause.

Answer: They Sold All Their Cars

The standard way to run a car rental business is to borrow some money, use it to buy a big fleet of cars, then earn money by renting those cars out to companies and individuals. Say your monthly loan repayments on a Fiat Panda are €250 per month, but you charge a rental price of €100 per week. As long as you’re renting it out for 3 weeks of the month, you’re in business. Across your whole fleet, the difference should be big enough to pay staff, buildings and other costs, and some profit for yourself too.

In 2020, as the pandemic hit and almost all international travel ground to a halt, this model became very unviable. As long as you owned the cars, you had to make the monthly repayments, but there were no more Americans coming to discover their ancestors, so your Fiat Panda was rented for zero weeks in a month. So you’d have to borrow more money, work out a deal with the bank or sell the car to cover the loan.

According to the Car Rental Council of Ireland, there were about 21,500 rental carsin Ireland as the pandemic hit. By the start of 2022 there were 10,000. They sold over half of the national fleet.

I don’t know much about the rental car market, but I assume a level of buying and selling to match your fleet size to seasonal travel trends is normal, so this might have seemed precarious, but not crazy, at the time.

They Can’t Buy New Cars

As the summer of 2022 approaches, tourism numbers are returning to pre-pandemic levels, but the car rental companies are struggling to replenish their fleet. They bought 697 new cars in Jan 21, for example, but only 369 this January.

The main cause here is that, ironically, the car manufacturers also took an over-sized reaction to the start of the pandemic. When they closed their factories in March 2020, they cancelled all of their orders for microprocessor chips. Or, more importantly, they cancelled their place in the queue for microprocessor chips. Consumer electronics companies jumped in and took their place in the queue, and the queues got longer as chip production itself was also slowed by the pandemic.

All this meant that once car manufacturing plants re-opened, they were at the very end of a very long queue. Add in Brexit and other pandemic supply chain issues, and Ireland imported only 63,317 cars in 2021, compared with 113,926 car imports in all of 2019.

There are other potential compounding factors, such as reports that car dealerships are preferring to sell their limited supply of cars to retailers (at full price) rather than to rental companies (in bulk, at discount), or that so few cars got purchased during the great recession a decade ago, there there is now far fewer second hand cars on the market than normal.

What Next?

As always with inflation, price is the symptom, not the cause, so price caps or price control won’t solve the underlying problem. Or, more accurately, they will just switch the situation from “highest bidder gets the car” to “first in line gets the car”, but it won’t increase the number of people able to rent cars this summer. It would reduce the profits of the car rental companies and keep money in the pockets of tourists, which is fine if that’s your goal, but that could hamper the ability and incentive to rapidly replenish supply.

With no obvious way to quickly increase the rental fleet, the prices are likely to remain high this year and probably next year too. I’m not sure if Government could have stepped in two years ago to provide credit to prevent this – the specifics of the bottlenecks were probably to hard to predict. Alternative supply will be key – including public transport, taxis, tour busses, all of which will feel extra strain from tourism this summer. In some instances, travel bloggers are even renting delivery vans as cheaper alternatives.

💡 Interesting Links

The Market for Electricity Production

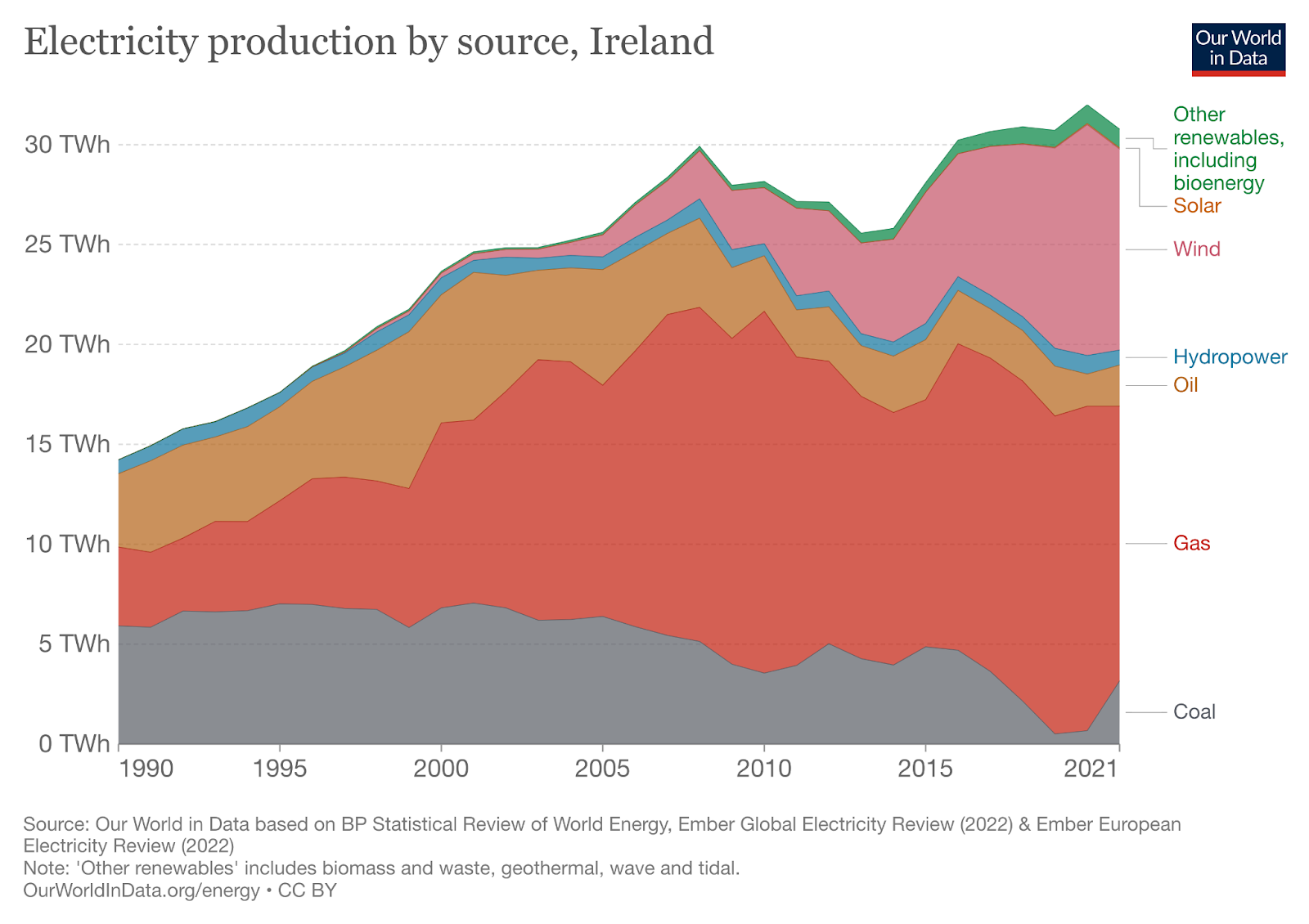

In the UK, during the ad break for Deal or No Deal, or at half time in an England game, so many people go to boil the kettle at the same time that the national grid needs to plan for huge surges of energy demand. Spikes like this (called TV Pickup) make it very difficult to balance supply and demand in an energy market, and present challenges as we move to sustainable (but less consistent) sources like wind and solar.

Fergus McCullough has an interesting writeup on the market for electricity production in Ireland. Renewables came from almost nowhere in 2008, to 43% of production in 2020 (image below), but gas still acts as the backbone of supply, able to ramp up and down for every ad break of the Late Late.

Why Income Taxes Were Unexpectedly High

The top rate of income tax in Ireland is 40%. Higher actually, when you include USC and others, but I’ll stick to the simple numbers for this example. If you earned €50,000 last year you didn’t, however, pay 40% of that as tax. This is because we have a progressive tax system, so you pay different tax rates on different portions of income. In this example, you would have paid 20% tax on your first €35k – which is about €7k. You’d only pay a 40% tax rate on the remaining €15k – which is about €6k.

So even though your top rate of tax is 40%, you’d only pay about €13k in tax, which is a 26% effective tax rate. (No more maths after this, promise!)

However, if you got a €5k pay rise last year (congrats!) all of that extra €5k would be taxed at the top rate of 40%. By definition, all salary increases are taxed at your highest rate.

If somebody on a €20k salary got the same €5k tax rate, they would only pay the lower rate of 20% on that raise, as their new salary is still under the threshold.

In 2021, the Irish state collected €4 billion (17%) more in income taxes than was planned for in the budget. Caoimhín Ó Tiománaigh has done some great analysis on this, published in a full report and as a tweet thread, but the summary is that, like in our example above, lots of people got salary increases (and new jobs) and paid the highest available tax rate on them.

This was unexpectedly high, and because all salary increases happen at the margin, the level of income tax collected rose even faster than wages did. Most of this increase happened in higher earning jobs, at the higher rate of tax, so the effect on taxes collected was even more amplified.

As recovery continues into the future, however, it might happen mostly in lower wage sectors (i.e. service industry getting back on its feet), so the report cautions against banking on this outsized effect on income taxes to to continue.

Continued Spiral or Soft Landing?

David McWilliams makes a fairly stark, and grim prediction that inflation will continue at pace in Ireland, followed by a recession. In the US the Federal Reserve is raising interest rates, which will raise the cost of borrowing (including mortgages) and many economists predict this will soften the growth in house prices. McWilliams doesn’t believe the same will happen here, with Ireland’s inflation decoupled from mainland Europe and the ECB unwilling to raise rates because of high energy costs. He predicts house prices (and prices more generally) will continue to soar. It’s 2004 all over again.

Noah Smith is predicting the opposite for the US – a soft landing with a small recession. He shares a few reasons which I thought would be interesting to list below and contrast with McWilliams’ predictions for Ireland:

1. As mentioned above, the US Fed is raising interest rates, and the property market is already showing signs of cooling. Since McWilliam’s article was published, the ECB has signalled potential interest rate increases, but small ones, so that’s a small plus for the “soft landing” column here.

2. In the US, The COVID stimulus has stopped and people are finished spending the money they saved during lockdown. In Ireland, PUP ended in March, and savings levels have dropped in half, but they’re still much higher than the US and spending shows no sign of slowing down. + 1 for McWilliams.

3. Central bank lending in the US is down and the government ran a surplus in April (a.k.a “implemented austerity”), both of which remove inflationary pressure and neither of which are true here.

Comparing both sets of logic, I think McWilliams’ prediction is directionally correct, but the ECB rate increases might (hopefully) soften the blow.

🎧 Podcasts

This week I’ve started listening to Hot Mess, on the Climate Crisis in Ireland, by Philip Boucher-Hayes and RTE.